Primary factors insurers use to set prices

Insurers set green slip prices and State Insurance Regulatory Authority (SIRA) regulates those prices. Insurers use different factors and apply their own weightings to these factors to set the prices they will charge.

Certain factors used by insurers affect green slip prices more than others.

Factors that affect green slip prices

| Owner and vehicle | Driving and claims record |

|

Geographic region |

Driving record: |

|

Type and age of vehicle |

|

|

Vehicle performance |

|

|

Distance travelled |

|

|

Motor insurance held |

Claims history: |

|

Age of vehicle owner |

|

|

Age and gender of youngest driver |

|

Five rating regions

SIRA designates geographic or rating regions and vehicle classifications.

There are 5 geographic or rating regions:

- Sydney Metropolitan

- Outer Metropolitan

- Wollongong

- Newcastle/Central Coast

- Country.

Insurers are not allowed to differentiate prices on the basis of postcode within a rating region.

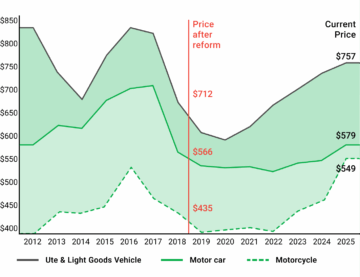

Green slip prices vary

In the past 12 years, green slip prices have varied considerably. This makes it more important than ever to compare green slip prices.

Average green slip prices at June 2012 to 2025

Average green slip prices by type of vehicle

|

At June |

Motor car |

Ute/LGV |

Motorcycle |

|

2012 |

$575 |

$843 |

NA |

|

2013 |

$616 |

$764 |

$437 |

|

2014 |

$608 |

$724 |

$429 |

|

2015 |

$662 |

$793 |

$447 |

|

2016 |

$689 |

$841 |

$535 |

|

2017 |

$695 |

$833 |

$465 |

|

2018 |

$566 |

$712 |

$435 |

|

2019 |

$535 |

$661 |

$406 |

|

2020 |

$531 |

$651 |

$412 |

|

2021 |

$535 |

$675 |

$414 |

|

2022 |

$521 |

$705 |

$405 |

|

2023 |

$541 |

$736 |

$439 |

|

2024 |

$546 |

$735 |

$462 |

|

2025 |

$579 |

$757 |

$549 |

How SIRA regulates green slip prices

As the regulator, SIRA must ensure the scheme is competitive and green slips are affordable:

- The scheme is competitive only if a sufficient number of insurers are motivated to participate.

- Insurers participate only if there is sufficient profit.

Insurers must first submit proposed prices to the regulator SIRA, setting out proposed premiums and supporting information.

- Insurers must submit prices to SIRA at least once a year.

- They may submit a non-compulsory filing if they wish to vary premiums at other times during the year.

SIRA may reject these proposed prices if it considers they:

- will not fully fund the insurers liability

- are excessive, or

- do not conform with Premiums Determination Guidelines.*

* SIRA issues Premiums Determination Guidelines to regulate how green slip prices are set. SIRA also regulates distribution and marketing of green slips through the Market Practice Guidelines. Both are in the Motor Accident Guidelines 2017, available from SIRA.

SIRA also operates a price comparison service, Green Slip Price Check.